.jpg)

Almost 1,500 lawsuits have been filed by policyholders against insurers, seeking to resolve disputes around insurance coverage for COVID-19-related business losses.

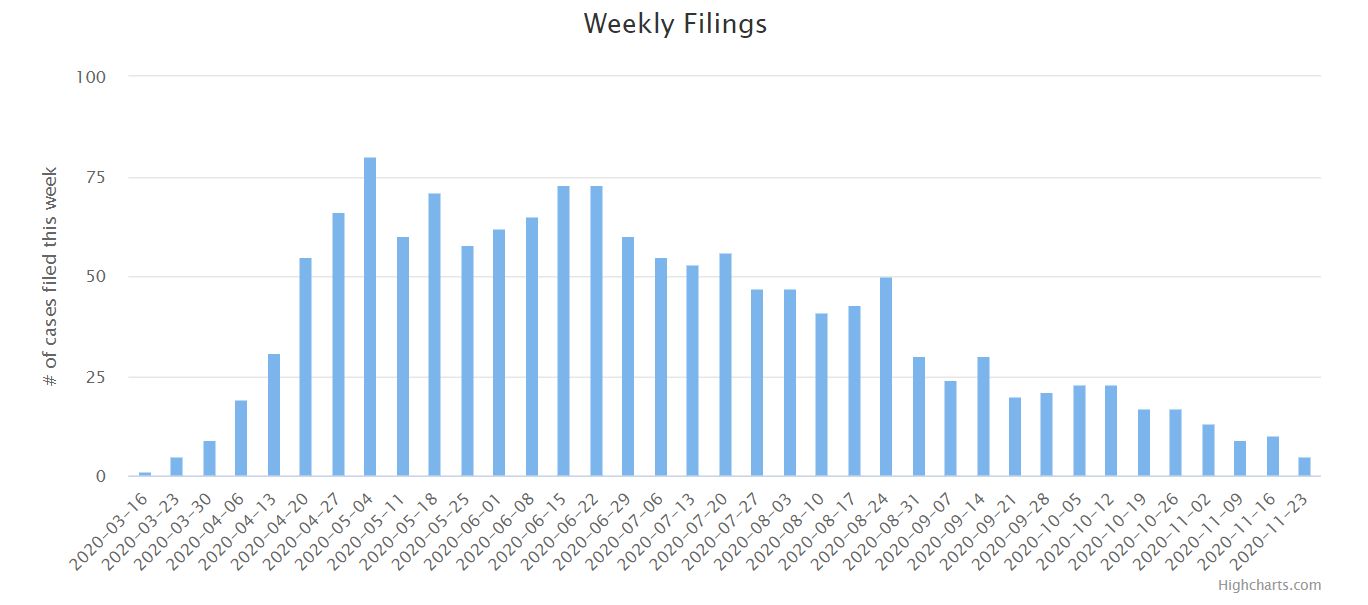

For those unfamiliar with insurance litigation trends, it’s important to put the scale of this into perspective. The average hurricane will result in about 50 to 100 cases being filed in the first year; from April till August 2020 we saw the same quantity of cases being filed each week for COVID-19-related losses.

So far, rulings have been made overwhelming in the favor of insurers, at a rate of approximately 75%. However, there have been some significant rulings in favor of policyholders over the last few months which should cause insurers pause for thought.

An Overview of the Numbers

The University of Pennsylvania Carey Law School has been maintaining a COVID Coverage Litigation Tracker since the beginning of the pandemic, which provides us with a wealth of data to analyze.

Weekly filings peaked from mid-March until late August 2020 and then began to tail off towards the end of the year.

Graph courtesy of The University of Pennsylvania Carey Law School

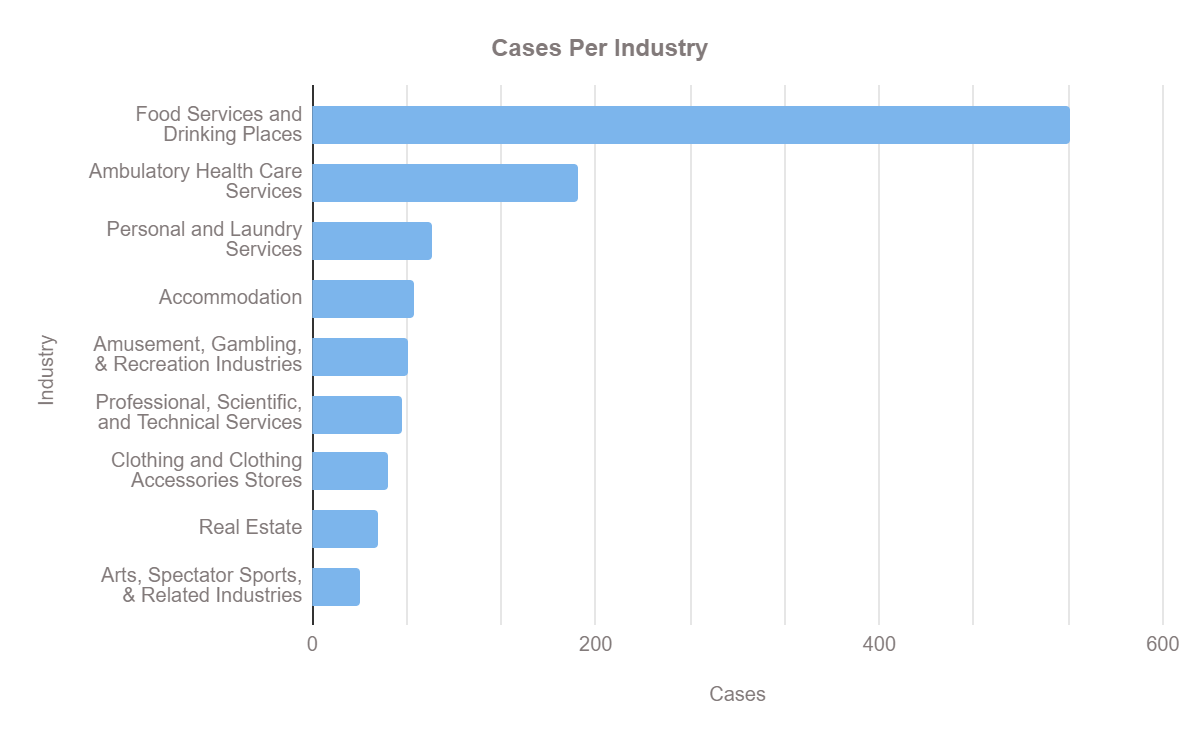

The industries that these cases are emanating from are all industries that have been adversely impacted by government stay-at-home orders, with 38% of all cases being brought by policyholders in the food and drink industry.

Graph courtesy of The University of Pennsylvania Carey Law School

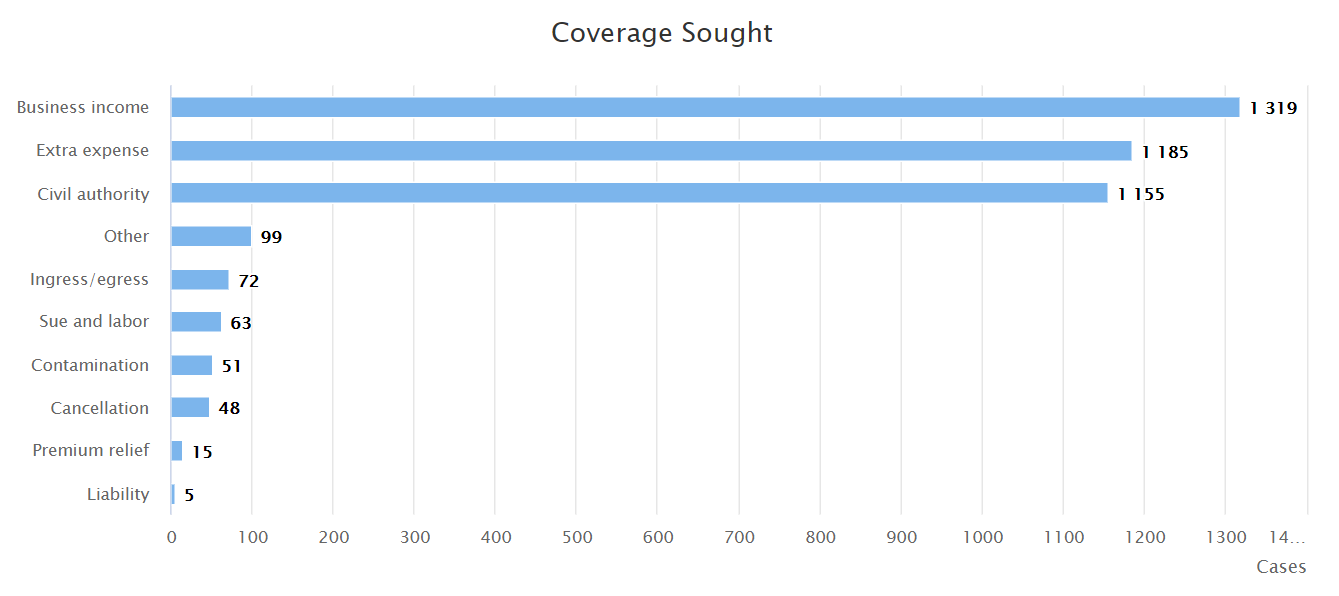

The vast majority of plaintiffs are claiming coverage provided within a Business Interruption (BI) policy. And there are principally three sections of cover within a BI policy where plaintiffs are seeking coverage: business income, extra expense, and civil authority.

Graph courtesy of The University of Pennsylvania Carey Law School

The Arguments

Given the number of cases filed combined with the fact we’re starting to see some judgments trickle through, there are a number of common arguments emerging among both plaintiffs and defendants.

Policy exclusions for viruses

Some of the plaintiffs’ BI policies contain clear exclusions for viruses. In these instances, insurers are often succeeding by bringing early motions to dismiss.

Out of the 86 cases that have so far had a motion to dismiss granted, 65 of these contained a virus exclusion in the policy.

Prominent cases include Chattanooga Professional Baseball LLC d/b/ Chattanooga Lookouts et al. v. Philadelphia Indemnity Insurance Co., et al. where in November a federal judge in Arizona granted the motion to dismiss, citing the virus exclusion. Meanwhile, also in November, a California superior court judge dismissed the plaintiff’s case in Musso & Frank Grill Co. Inc. v. Mitsui Sumitomo Insurance USA Inc., citing the virus exclusion as a factor in the judgment.

However - the existence of a virus exclusion in a policy hasn’t always resulted in success when an insurer has brought an early motion to dismiss. In Urogynecology Specialist of Fla. LLC v. Sentinel Ins. Co. the judge ruled that the virus exclusion was not unambiguous enough to bar coverage being sought by the plaintiff.

While the policy excluded claims caused by “the presence of fungi, wet rot, dry rot, bacteria or virus.”, the judge ruled that denying coverage for COVID-19 "does not logically align with the other pollutants" that the “policy necessarily anticipated and intended to deny coverage for these kinds of business losses.”

What constitutes a “direct physical loss”?

For policies that do not contain a virus exclusion, the next line of argument is what exactly constitutes a “direct physical loss”, and it is this question that courts are now having to rule on.

Most BI policies require “physical loss of or damage to property” in order for an insured’s loss to be covered. For example, if a hurricane damages a restaurant’s premises to the extent it’s unable to reopen until repairs have been completed, then this constitutes a direct physical loss (structural damage) caused by an insured event (inclement weather).

Insurers are therefore leaning heavily on the definition of the term “physical”, which they are arguing means physical damage or alteration to the property, rather than just economic loss that is unaccompanied by physical damage.

Most rulings in favor of insurers, where policies do not contain virus exclusions, have been based on this definition of “direct physical loss”.

In the very first COVID-19-related insurance case to reach a judge, Gavrilides Management Company, et al. v. Michigan Ins. Co., back in July 2020, the Michigan state court judge ruled in favor of the insurer, rejecting the argument from the policyholder that the loss of use of the property caused by government restrictions constituted a direct physical loss.

Therefore, the judgement concluded that the loss of use or access to a building does not in and of itself, constitute “direct physical loss or damage”.

Policyholders have of course been developing arguments to counter this, which assert that virus particles have caused physical damage to property or that structural alteration to a property is not required in order to sustain a direct physical loss. Significant rulings on these cases are explored below.

Rulings to Date and Significant Cases

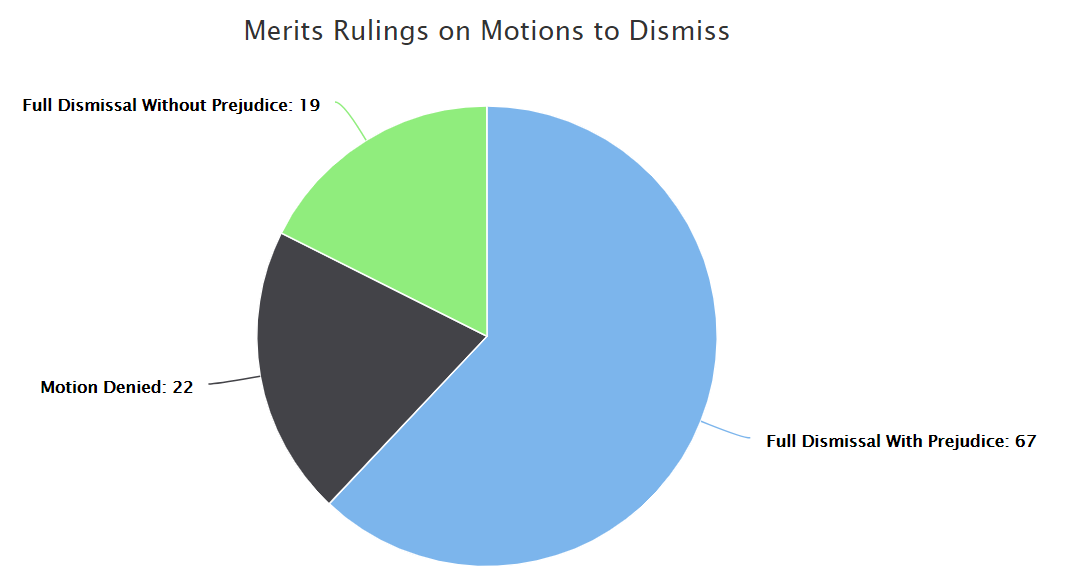

So far, most cases have only got to the pre-dismissal stage, where insurers are challenging around 25% of all cases with early motions to dismiss. And insurers are coming out on top here, overwhelming so, with a success rate of almost 75%.

Graph courtesy of The University of Pennsylvania Carey Law School

However, of the handful of cases that have had the motion to dismiss denied, we now have a few clear precedents which will undoubtedly have an impact on future litigation strategies.

Studio 417 v. Cincinnati Insurance Co.

One of the first rulings in favor of a policyholder came in August 2020, when a federal judge in Missouri allowed the suit to proceed. In this case the plaintiffs, a group of hair salons and restaurants, argued that the physical presence of COVID-19 virus particles within their business premises damaged their property and amounted to direct physical loss, pursuant to their policies.

The court decided that “loss” could be defined as “loss of use” as the trigger wording within the policies was "direct physical loss of or damage to" covered property.

However, it should be noted that this ruling merely allowed discovery to continue and it did not decide the coverage issue of whether the plaintiffs argument did in fact constitute direct physical loss.

Optical Services USA/JCI v. Franklin Mutual Insurance

In this case, heard in September 2020, a group of New Jersey optometrists built a different argument than Studio 417, as they did not allege that there were physical COVID-19 particles on their premises. They instead argued that this was not necessary to establish coverage and that New Jersey case law asserts that structural alteration to a property is not required in order to sustain physical loss.

The plaintiffs cited judgements from two similar cases. In Gregory Packaging Inc. v. Travelers Property Casualty Co. of America, 2014, a federal court in NJ ruled that ammonia gas discharge into a building rendered the property “temporarily unfit for occupancy” and therefore amounted to direct physical loss. And in Wakefern Food Corp. v. Liberty Mut. Fire. Ins. Co., 2009, where a court ruled in favor of a grocery store seeking coverage following an electrical outage caused by a fault in the grid.

The court concluded that based on the case law cited, the insurance policy definition of the term “physical” should be more encompassing than simply “material alteration or damage” to property and determined that the plaintiffs were entitled to issued-oriented discovery.

North State Deli, LLC v. The Cincinnati Insurance Co.

This case is the most significant to date, as unlike the above, this was a declaratory judgement, rather than a motion to dismiss.

A group of restaurants located in North Carolina brought a declaratory judgement action against The Cincinnati Insurance Company and The Cincinnati Casualty Company, having been denied cover for their COVID-19-related BI claim.

The insurers denied the original claim, arguing that loss of the physical use of and access to the policyholders’ restaurants did not constitute a direct physical loss as pursuant to the insurance policies.

However, the North Carolina state court examined the policies alongside dictionary definitions of “physical” and ruled in favor of the plaintiffs, arguing that “the ordinary meaning of the phrase ‘direct physical loss’ includes the inability to utilize or possess something in the real, material, or bodily world, resulting from a given cause without the intervention of other conditions.”

Conclusion

The decisions in both Optical Services USA/JCI and North State Deli, LLC are significant for two reasons. Firstly, no clams were made by the plaintiffs that the COVID-19 virus was physically present within their business premises. Secondly, and most importantly, the judgements support a broader definition of “direct physical loss”, beyond simply structural alteration to a property.

Both of these judgements will no doubt impact plaintiffs’ strategies as more and more cases make it to court. The success of these strategies, however, remains to be seen.

This blog post is not offered, and should not be relied on, as legal advice. You should consult an attorney for advice in specific situations.

Gary Markham is the founder of AI-enabled predictive analytics legaltech company LSG, who provide enterprise-level litigation and panel counsel management software to insurers.

Related Content:

1. Understanding Insurance Policies and Potential Insurance Recovery After Covid-19

2. Insurance Coverage for Coronavirus: Mitigating Loss and Protecting the Business

3. Recent Litigation of Force Majeure and Other Contract Defenses During COVID-19

.jpg?width=352&name=assaultclaims%20(1).jpg)

.jpg?width=352&name=D%26OLetter%20(1).jpg)